Watch for it—Advanced nuclear “liftoff” needs 5–10 reactor contracts by 2025

March 31, 2023, 9:29AMNuclear News

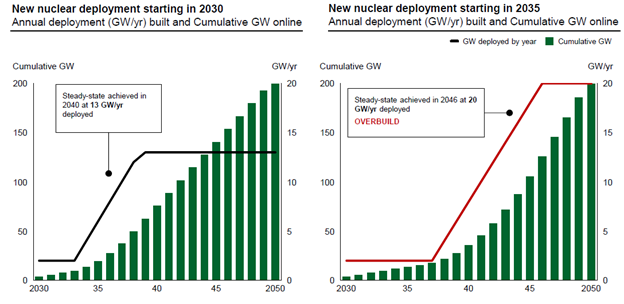

These graphs illustrate how rapidly scaling the nuclear industrial base would enable nearer-term decarbonization and increase capital efficiency, versus a five-year delay to reach the same 200 GW deployment by 2050. (Source: DOE, Pathways to Commercial Liftoff: Advanced Nuclear, Fig. 1)

The Department of Energy released Pathways to Commercial Liftoff: Advanced Nuclear earlier this month. It is one of the first in a series of reports on clean energy technologies and the private and public investments needed to overcome hurdles to full-scale deployment. The report makes a clear case for investment in nuclear power and challenges potential investors and operators to move beyond the current “wait and see” stalemate and generate “a committed orderbook . . . for 5–10 deployments of at least one reactor design by 2025.”

To continue reading, log in or create a free account!